Benefits of Owner Financing for Home Buyers

- Raquel Gutierrez

- Nov 15, 2025

- 10 min read

Owner financing is a unique home buying strategy that offers several benefits for both buyers and sellers. It allows buyers to purchase a home directly from the seller without needing a traditional bank loan. This can be a great option for those who struggle to qualify for conventional mortgages.

In owner financing, the seller acts as the lender, and the buyer makes payments directly to them. This arrangement can offer more flexible terms and conditions compared to traditional loans. Buyers often find this method appealing due to its potential for faster closing times and less stringent credit requirements

However, it's important to understand the risks involved, such as the possibility of default. Both parties should have a clear, legally binding agreement to protect their interests. Owner financing can be a win-win solution if both parties understand and agree to the terms.

What Is Owner Financing? Understanding the Basics

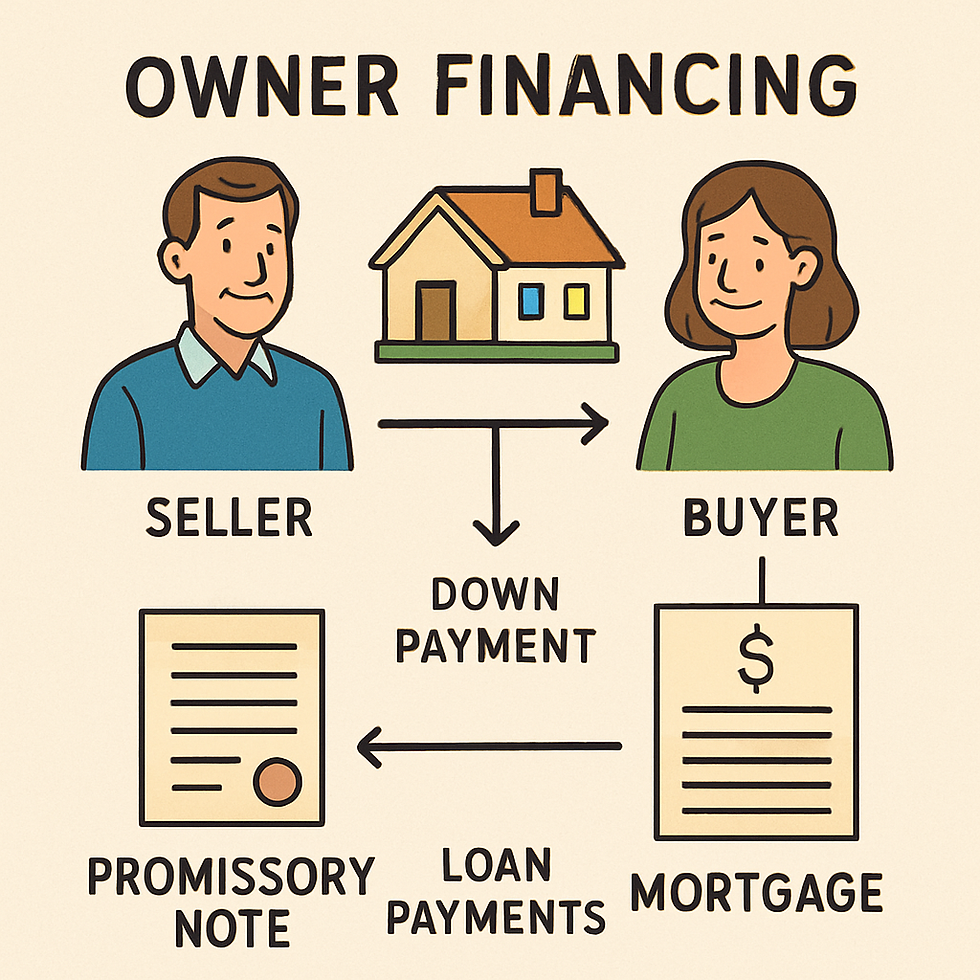

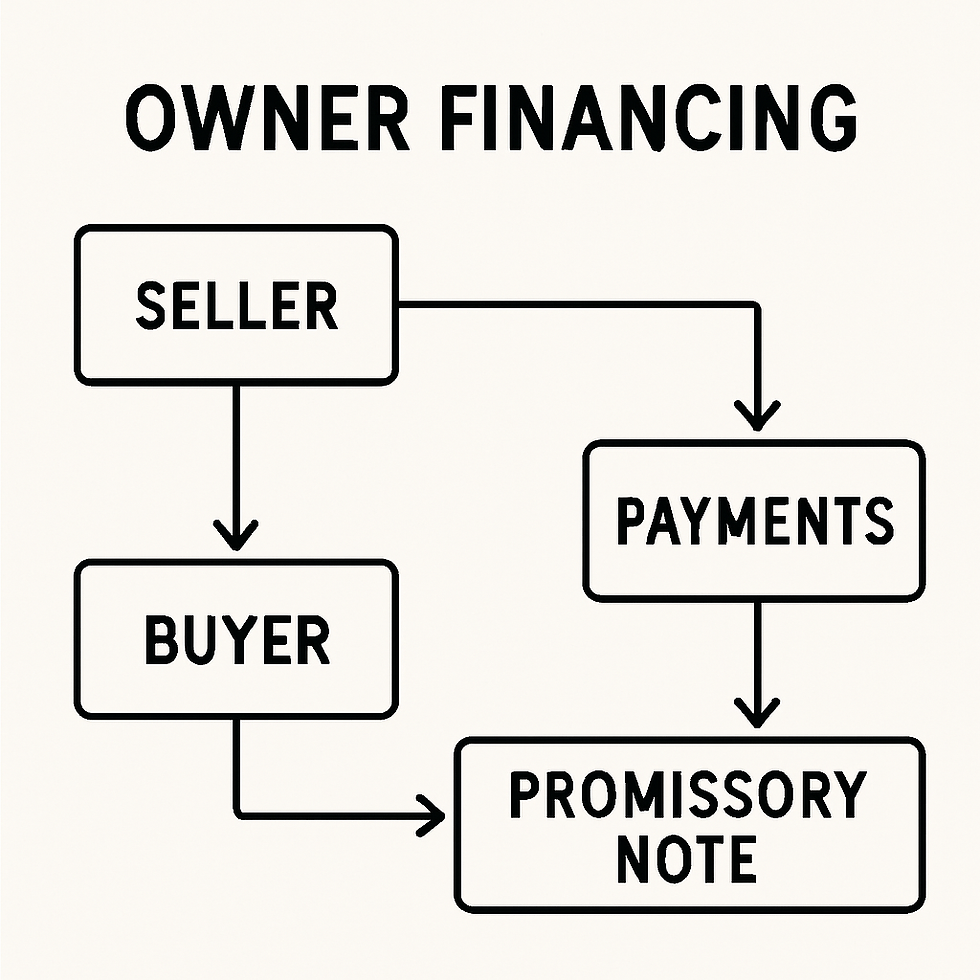

Owner financing, also known as seller financing, lets buyers purchase a home directly from the seller. This approach bypasses traditional bank financing. It is often used when buyers cannot secure a conventional mortgage.

In this setup, the seller becomes the lender. The buyer makes monthly payments to the seller instead of a bank. Typically, a formal contract details terms such as interest rates, repayment schedules, and consequences of default.

Here’s a simple breakdown of key features:

• Buyer and seller agreement: The terms are negotiated directly.

• No bank approval needed: Streamlines the buying process.

• Flexible terms: Customizable to fit both parties' needs.

Owner financing can apply to various properties, including homes and land. It offers an opportunity for buyers to own property when conventional financing isn't an option. While it offers flexibility and faster closure, it's vital for both parties to fully grasp the financial and legal implications. This understanding ensures a smooth transaction and minimizes potential disputes.

How Does Owner Financing Work? Key Steps and Structure

Owner financing involves several crucial steps, creating a structured path for the transaction. First, both buyer and seller agree on the sale price and terms like down payment, interest rate, and repayment period. These terms are vital as they set the financial expectations for both parties.

Next, a formal contract is prepared. This document should clearly outline all conditions, ensuring mutual understanding. Both parties need to scrutinize this contract before proceeding. This ensures that there are no hidden surprises later on.

The buyer then pays the seller directly, typically on a monthly basis. The seller holds the promissory note, acting as a lender. Usually, the buyer gets the deed after fulfilling the loan terms, but the seller retains a lien until then.

Throughout this process, clear communication and proper documentation are essential. They safeguard interests and ensure a seamless transaction between buyer and seller. Understanding each step helps in mitigating risks and encourages a successful home purchase through owner financing.

Types of Owner Financing Arrangements

Owner financing can be structured in various ways, each catering to different needs and circumstances. The most common types include the land contract, lease-purchase agreement, and seller carryback mortgage. Understanding these options can help buyers and sellers choose the best fit.

A land contract involves the buyer making payments over time while the seller retains the title. This option is often used for owner financing on land, where the land deed is transferred after the final payment.

Basically, with a lease purchase agreement, you start off renting the house. The cool part is that the contract includes the choice to buy the house down the road. It's a great way to 'test drive' the home and neighborhood while you get your finances in order to buy it.

A seller carryback mortgage is where the seller acts as the bank, providing a loan directly to the buyer. This method involves the buyer paying back the seller in installments over a specified period.

Here are the common types of owner financing:

1. Land Contract: Title transfer after full payment.

2. Lease-Purchase Agreement: Rent with an option to buy.

3. Seller Carryback Mortgage: Seller provides financing.

Exploring these arrangements helps find the right approach. It is essential to weigh the benefits and potential drawbacks of each type. This knowledge aids in making informed decisions in owner-financed transactions.

Advantages of Owner Financing for Home Buyers

Owner financing offers several benefits that can make home buying more accessible and flexible. This arrangement can be particularly advantageous for buyers who face challenges with traditional loans.

One major advantage is the flexible terms that owner financing can provide. Buyers and sellers have the freedom to negotiate terms, such as interest rates and repayment schedules, that suit both parties.

Owner financing can also expedite the home buying process. Without the need for lengthy bank approvals, buyers might close deals faster, securing their new homes sooner than through conventional means.

Credit issues are often a stumbling block in traditional financing. Owner financing can be an excellent alternative for those with poor credit, as sellers may be more understanding of diverse financial backgrounds.

Another big plus is that you're often buying straight from the owner, which really cuts down on extra costs. You get to skip all those bank fees and other 'middleman' expenses, making the whole deal much cheaper.

Also, when the owner finances the deal, the payment plan is usually very flexible. Instead of a bank's strict rules, the plan can be tailored to your specific situation. This just means you work out payments that you can actually manage and comfortably afford.

These advantages make owner financing a viable option for many buyers seeking alternative home buying strategies.

Potential Risks and Considerations for Buyers

While owner financing can offer many benefits, it's important to be aware of potential risks. Buyers need to consider several factors before entering into an owner financing agreement.

One primary concern is the possibility of higher interest rates. Buyers might pay more over time compared to traditional loans, impacting overall financial health.

Another risk involves the potential for the buyer to default. If payments aren't met, the buyer risks losing the property, and foreclosure could follow.

The lack of a traditional lender means there's less regulatory oversight. Buyers need to ensure all agreements are clear and legally sound to avoid future disputes.

There can also be challenge concerning the property's title. Buyers should verify the property is free from liens and encumbrances to ensure a smooth transaction.

It's really important to understand all the risks and take steps to protect yourself. Every buyer's situation is different, so you have to think carefully about your own circumstances to make sure the deal is successful.

This isn't just for houses!

Owner financing is great because it's not just limited to standard homes. It's a fantastic, flexible option if you're looking to buy land or other unique properties.

It's especially useful for buying raw land. Why? Because regular banks often refuse to give loans for land. They see it as a risky, 'speculative' investment. When banks say no, owner financing is often the perfect alternative.

The same goes for unique properties think of a historic home with special rules or a building with a really unconventional design. Banks have a very strict checklist, and these kindsof places don't fit in their box. Owner financing lets you bypass all those strict bank rules.

But.. Do Your Homework First

You must do your 'due diligence' which is just a fancy way of saying "do your homework". Before you commit to anything, you need to understand all the rules for that property. This means checking:

• Zoning laws: What are you legally allowed to build or do there?

• Environmental regulations: Are there any environmental issues or protections?

• Land use restrictions: Are there any other limits on how you can use the property?

So, the key things to remember are that it's a great option for raw land, a good fit for unique properties, and you must always do your background research.

The bottom line is that owner financing opens up a lot more real estate options for you. It gives you the flexibility to get creative and make a purchase that wouldn't be possible with a bank.

So, how is this different from a regular bank loan?

It's crucial to understand the main differences between owner financing and a traditional mortgage so you can pick what's best for you.

Who is the lender?

• Traditional Mortgage: A bank or other financial institution lends you the money.

• Owner Financing: The seller acts as the bank. They are the one lending you the money.

How fast is it?

Owner financing is usually much faster. You get to skip the whole lengthy bank approval process. Since you're just dealing with the seller, the transaction can close very quickly, which is great for both of you.

How flexible is it?

This is the biggest advantage. Banks have very strict, 'one-size-fits-all' rules. With owner financing, the terms are completely negotiable. You and the seller can customize a plan that fits both of your unique financial situations perfectly.

Selecting between owner financing and traditional mortgages depends on specific financial situations and preferences. Understanding these key differences will aid in making an informed decision.

What Happens If the Buyer Defaults? Protections and Consequences

Defaults can happen even with the best plans. Understanding the consequences of a buyer defaulting in owner financing is crucial.

When a buyer fails to meet payment obligations, the seller may need to take action. This could include starting foreclosure procedures to reclaim the property.

Sellers should establish protections in the owner financing contract to address potential defaults. These might include specifying conditions under which foreclosure can begin and any grace periods allowed.

It's vital for both parties to be aware of the default consequences. Sellers should ensure they have legal safeguards in place, while buyers need to understand their obligations to avoid defaulting.

Key protections and consequences include:

1. Foreclosure initiation if payments are missed

2. Possible grace periods for payments

3. Legal clauses specifying default conditions

4. Having a clear understanding of these elements helps mitigate risks associated with defaults in owner financing agreements.

How to Negotiate and Structure an Owner Financing Agreement

Negotiating an owner financing agreement requires a keen understanding of both parties’ needs. Start by clearly outlining terms such as the interest rate, down payment, and loan duration.

Flexibility is key. Both the buyer and the seller should be open to customizing the agreement to fit individual circumstances. Discuss potential adjustments before finalizing anything.

A good, solid agreement must be crystal clear about what happens if you pay late or, worse, if you default (which means you stop paying). These rules need to be spelled out explicitly so there are no "I didn't know!" arguments later on.

Don't try to do this yourself.

To make sure the whole deal is legal and fair, you should always hire a real estate lawyer. They know how to write up a proper contract that includes all the terms you and the seller agreed on and, most importantly, follows all the local laws.

A proper contract should always clearly answer these questions:

Money: What's the down payment? What's the interest rate?

Schedule: What's the payment plan (how much, how often)? And how long will you be paying for?

Default: What exactly happens if you fail to pay? What are the legal steps and consequences?

Bringing in a professional (like a lawyer) is the best way to create a balanced agreement that protects both you and the seller. That’s the real secret to making an owner financing deal work out well for everyone.

The Legal & Tax Stuff (Don't Skip This!)

You really need to understand the legal and tax side of owner financing. This is crucial for both the buyer and the seller because it can lead to some great tax benefits... or some big, expensive problems.

1. The Legal Part (Get a Lawyer!)

Legally, the most important thing is the contract. It has to be incredibly detailed and clearly spell out every single term you agreed on. This is not something you should download from the internet or write yourself.

You must hire a real estate lawyer. They will make sure the contract is fair, protects you, and follows all the local laws.

2. The Tax Part (Get an Accountant!)

The tax rules can change depending on your deal (like the interest rate or loan length).

For Sellers: There’s a potential big win. You might be able to use an "installment sale" for your taxes. This just means you get to spread out the profit you made over many years. Instead of paying one huge tax bill in one year, you pay it in smaller bits as you receive the payments.

For Buyers: You can often deduct the interest you pay to the seller on your taxes, just like you would with a regular bank mortgage.

Both of you need to know exactly what to report on your tax returns.

Honestly, you should talk to a tax professional (like a chartered accountant). They can explain the exact financial impact on your situation and make sure you're doing everything by the book.

Got Questions? Here Are Some Common Answers (FAQ)

People always have a ton of questions about owner financing. Let's clear up a few common ones.

Q: What is owner financing, really?

A: It's simple: the seller acts like the bank. You pay them directly every month, instead of getting a loan from a traditional bank.

Q: Is it actually a good idea?

A: It definitely can be! It's a fantastic option for buyers who have bad credit or 'unusual' income (like freelancers) and can't get a bank loan. It's also great for sellers who just want to sell their property fast.

Q: What's in it for the seller?

A: The seller gets a steady stream of income (your payments). They also keep a legal claim (a 'lien') on the property as security until you've paid it all off.

Q: What happens if the buyer stops paying (defaults)?

A: This is serious. The seller has the legal right to foreclose and take the property back, just like a bank would.

People also ask a lot about:

• Can you do this if the seller still has a mortgage?

• Who actually holds the property's deed (title)?

• What are the biggest risks?

Knowing the answers to these is the first step to making a smart choice.

So, Is It a Good Idea? And Who Is It Really For?

This can be a really smart move, especially for people who struggle to get a normal bank loan.

Think about:

• People with bad credit or a tricky financial history.

• Freelancers, gig workers, or self-employed folks whose income isn't a simple monthly paycheck.

• Sellers who just want a fast, simple sale without bank delays.

But, you have to look at the good and the bad. Before you jump in, think hard about:

• Your real financial situation right now.

• The exact deal the seller is offering (is it fair?).

• Your long-term plan (e.g., will you try to get a real bank loan in a few years to pay the seller off?).

Bottom line: there's no single "yes" or "no" answer. It's a good idea if it fits your personal needs and you've done your homework.

Final Thoughts: How to Make This Work for You

Owner financing is a great, flexible option that helps people who don't fit the bank's perfect "profile" buy a home.

The most important thing you can do is understand all the details. Do your own research. Talk to a real estate expert.

And most of all: Get everything in writing. Make sure all the terms are crystal clear in a legal contract. This is where a lawyer is your best friend they'll protect you from future problems.

If you're careful and smart about it, owner financing can be the key to getting your home. It's all about matching your goals with the right strategy.

Comments